2K10 Independence-Day Message

Reclaim liberty by ending "Fraud of Fed" now

by Dean Hazel, et al

Picking this up from my favorite Monroe, Michigan, Whigg, Dean Hazel. Dean, in response to a blog post from another advocate of honest money—Steve Zimberg, thought-provoking founder of Societism.org—comes back with a prescription from Constitutional considerations.

The blog appears to have originated from the Metro-Detroit Freedom Fellowship. I list the point/counterpoint in chronological order. — bw

Original Post by Steve Zimberg

Friends,

We all know about the first Great Depression. It actually lasted many years! The full extent of the one we face today, even with all its problems, has been largely hidden by the government helping ease the pain with trillions in bailouts. But what would the government need to do if another one came and it had no money left? The following might be our elected representatives' next plan.

Encourage each and every business and homeowner to grab a hammer and smash out a few of their windows. Just a little sacrifice for a very needed and worthy cause. Then pick up your phone and call in someone to fix it. It will absolutely stimulate the economy. When that stimulus wears off, we will all do it again and if necessary, smash our car windows too. For those really feeling the financial stress of paying for the repairs, the government will provide financing and tax credits. They'll even set up repair shops in vacant storefronts. And of course, charge a tax to anyone who leaves their window broken for over 30 days.

In the short run, it will stimulate the economy just like it did in past depressions. But in the long term we will have nothing to show for it except tons of more debt.

A better solution, get rid of those elected officials and tell them to break their own windows if it's such a good idea.

Thanks Frédéric Bastiat for inspiring me to rewrite your 1850s essay, "The Broken Window Theory,"— to draw a parallel to today's Keynesian stimulus plans by illuminating the notion of hidden costs associated with destroying property of others and the law of unintended consequences, in that both involve an incomplete accounting for the consequences of an action.[1]

Steve

First Reply by Dean Hazel

Dear friend,

Are you speaking of the Great Depression of 1893? There were more Great Depressions than just the one of 1929, you know! The results of bank loan scams like those of the Civil and immediate Post Civil War, which caused several 19th century depressions, were sanctioned into oblivion by our 14th Amendment to the US Constitution and was the reason that the certificate of the ratification of that amendment was falsified just as they were in both the 15th and 16th amendments.

Because the banks engaging in "Fictions to Cover Usury" were politically behind the falsification of amendments that were needed by them, to protect themselves from prosecution for their monetary frauds, that are just like the ones that they are committing today, by kiting checks for loans against bank float created by the deposit by the bankers, of the securities offered for those loans, in the absence of any real money being owned or loaned by our criminal banking system, the FRS. These words of the 14th Amendment tell it all!

"Section. 4. The validity of the [Fictions to Cover Usury] public debt of the United States, authorized by law, including [Fictions to Cover Usury] debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned."

The 15th Amendment was used to draw attention away from thislanguage in the 14th Amendment, and keep the focus of our nation instead upon race relations and civil rights when viewing the 14th Amendment. The 16th Amendment was meant and needed to provide the smoke and mirrors by which the inflation caused by the unprosecuted fraud upon borrowers could be retired as tax collections and kept more manageable so as to allow this type of usurious banking loan fraud scam to be perpetrated longer without discovery under the then new Federal Reserve Act.

That was why it was necessary to go so far as to falsify each of the certificates of ratification of the 14th, 15th and 16th Amendments, as exposed in the archived 1913 memoranda of the Solicitor of the Department of State, whose photocopy is displayed in the first volume of the two-volume book now being burned by the federal government, (Federal Mob), The Law That Never Was!

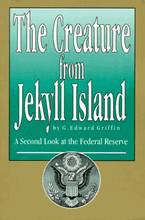

Banks should not be permitted to kite checks for loans against the securities offered by unsuspecting borrowers, who due to the indoctrination that passes for education, do not recognize such "Fictions to Cover Usury" on the part of the bank that is pretending to loan "money." Check kiting is the illegal act of taking advantage of the float to make use of non-existent funds in a checking or other bank account. How the inflation that this unprosecuted fraud upon borrowers creates is handled is explained in the first two chapters of G. Edward Griffin's book, "The Creature From Jekyll Island."

Griffin incorrectly refers to the "Fictions to Cover Usury" as "Checkbook Money!" Helping the bankers to hide both their fraud and usury! The US Constitution was written to protect US from such USURY! Sadly today with what now passes for an education, most all Americans do not know the distinct and intended differences our founding fathers knew, between coin, currency and money or that borrowing money meant that money would actually be loaned and not credit for money that does not really exist even through "Fictions to Cover Usury"!

Sincerely,

Dean S. Hazel

At this point, I [editor of Coffee Coaster, Brian Wright (bw)] requested to post as a guest column to both gentlemen. In my note to Dean, I stated that it was only recently I realized that housing loans from a bank generally do not represent any real asset held by the bank, only additional debt they are given by the Fed via the multiplier effect of fractional reserve banking. [In other words the "money" it loans is basically additional credit it gets courtesy the monopoly funny-money banking system.]

Steve replied to Dean that Steve was interested in gaining further insight into the history being cited.

Final Followup by Dean Hazel

Brian, Steve,

People should be vested in their homes and survive a foreclosure through what is called rescission of contract as the lender is without lawful consideration, i.e., "Real Money" formerly defined under 31 USC 314 and 315, or even US currency! For this reason I can say with complete authority that there is no national debt only a national fraud as there was no lawful consideration for the contract on the part of the conniving Federal Reserve System (FRS), our so-called national banking system.

The former 31 USC 314 and 315, now repealed by Congress—John Dingell and Carl Levin included—in support of the national monetary fraud and fictions to cover usury issued by and through our Federal Reserve Banking Cartel, read as follows (and should serve as a template for our Michigan State Attorney General to demand and sue our US Congress for the relief needed in our present situation under Article I, § 10 of the US Constitution, regarding the payment of debt):

31 USC § 314: Standard unit of value

The dollar consisting of gold nine-tenths fine as established by section thirty-five hundred and eleven of the Revised Statues of the United States [former 31 USCS § 315], SHALL BE THE STANDARD UNIT OF VALUE, AND ALL FORMS OF MONEY ISSUED OR COINED BY THE UNITED STATES SHALL BE MAINTAINED AT A PARITY OF VALUE WITH THIS STANDARD, and it shall be the duty of the Secretary of the Treasury to maintain such parity. (Emphasis Added)

"The Whigg Federation shall work for the rescission of money debt founded upon security fraud, and not founded upon a lawful consideration of money as established by the common law and historic statues of fraud of these United States of America."

As the remaining chairman of that organization, I am always working on this problem with that goal in mind. Too bad that many Republicans and Democrats are such dunderheads! The Democrats always accuse the Republicans of furthering the interests of banking and big business, though it was the Democrats that signed into law the Federal Reserve Act.

The term rescission of contract has a legal meaning as I use it adversarially, that may be found in the online legal dictionary at TheFreeDictionary.com.

Wrong or Default of Adverse Party

No Arbitrary right exists to rescind a contract. An executory contract that is Voidable can be rescinded on the grounds of Fraud, mistake, or incapacity.

A contract, whether oral or written, can be rescinded on the ground of fraud. The right to rescind for fraud is not barred because the defrauded party has failed to perform. Generally, false statements of value, or the failure to perform a promise to do something in the future without fraudulent intent, will not provide a basis for rescission for fraud or Misrepresentation. A party proves sufficient grounds for rescission by showing that he or she was induced to part with some legal right or to assume some legal liability that he or she otherwise would not have done but for the fraudulent representations.

On discovering the fraud, the victimized party can affirm the contract and sue for damages. He or she might instead repudiate the contract, tender back what he or she has received, and recover what he or she has parted with, or its value; the adoption of one remedy, however, excludes the other.

A contract obtained by duress can be rescinded, and in such a case, the same rules apply as in the case of fraud. A contract cannot be avoided because of duress or coercion, however, unless the duress was sufficient to overcome completely the will of the party who is seeking to avoid the contract.

A mutual mistake concerning a material fact entitles the party affected by the mistake to rescind the contract, unless the contract has already been completed and rescission would be an injustice to the other party. Rescission can also be allowed even for a unilateral, or one-sided, mistake in order to prevent an Unjust Enrichment of the other party [the BANK]. On rescission, the aggrieved party can recover the money he or she has paid or the property he or she has delivered under the contract [such as a mortgage note]. (Bracketed notes mine) —

TheFreeDictionary.com.

What we need is a wakeup call for more than a few candidates who are running for office and have been wrongfully blaming borrowers, our government and not the banks! Ron Paul and his son to my knowledge have not touched this one nor any other Republican candidates. Neither has Peter Schiff who should know this stuff. His father, Irwin, my friend who is serving time as a political prisoner of the Federal Mob, certainly knows this stuff inside out!

When you look at both the facts and law, you will more readily understand my words and outrage in the column that you, Brian, had posted for me on the bailout, when I first talk of jails, prisons and gallows. I say this because of some of the email that I had gotten from some of my fellow Republicans that in their denial are overly broad, blaming Obama as if only one man could be responsible for our long history of political banking fraud! And also blaming borrowers who shouldn't have been given loans and would not have been given loans if we had an honest banking system that loaned money instead of kiting checks against bank float for money that does not even exist by statutory definition as a standard of value!

Steve, Brian, I would welcome you for further discussions, to come to my Breakfast Club Meetings that will be held this month on Saturday the 10th and again on the 17th. Each meeting day is a Saturday for Monroe and the Bedford areas, respectively, on the second and third Saturdays of each month. Republican candidates and some of their promoters have been showing up. Sometimes it gets quite interesting.